European iGaming demand does not move only with how far a national team goes. In several markets, APS trends suggest that football culture, betting habits and tournament visibility can matter more than the final result.

Germany posted positive APS at every major tournament in the dataset, despite mixed sporting outcomes:

- +14.5% at WC 2018, despite a group-stage exit;

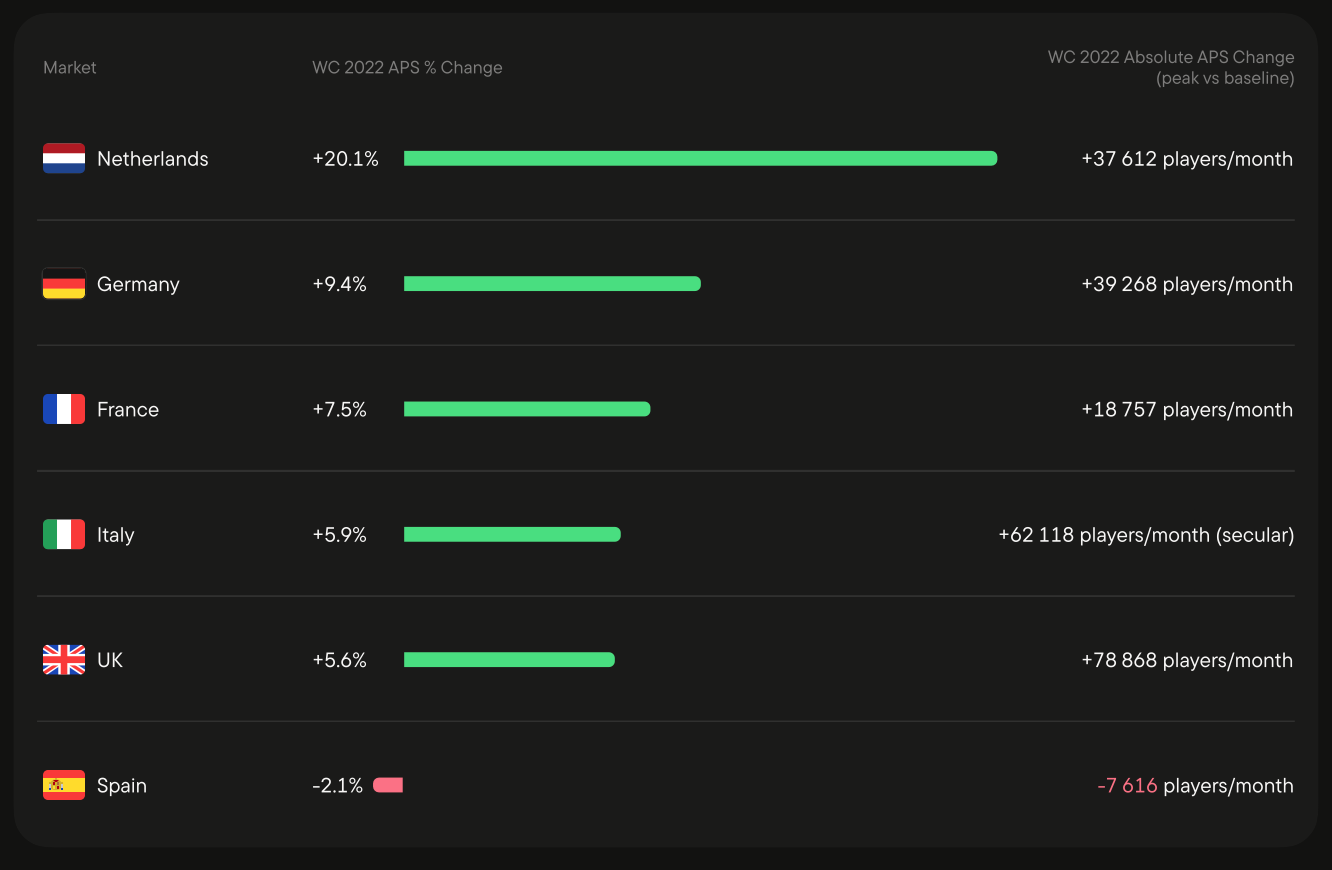

- +9.4% at WC 2022, despite another group-stage exit;

- +10.3% at Euro 2024, when Germany reached the quarter-finals as host.

That pattern suggests that tournament demand in Germany is not purely dependent on national-team performance. The event itself creates enough football attention to lift acquisition conditions.

The Netherlands shows the same point from another angle. It gained +17.8% APS at WC 2018 without even qualifying, then delivered the strongest result in the dataset at WC 2022, with +20.1% APS during its first World Cup as a licensed market.

Italy is the opposite case. Without a team on the pitch, Italian player engagement dropped below seasonal norms at WC 2018, with -15.2% APS. Even when Italy did participate but exited early at Euro 2024, the Blask Index still went negative, at -2.7%.

In other words, missing the tournament is not fatal for every market. In countries with strong football culture and active betting habits, the World Cup can still lift demand. But when a participating team exits early, the drop-off can be sharper because national attention has already been activated and then cut short.