Home Blog Blask x Ace Alliance Report: The US iGaming Market Shows Signs of Decline

Blask x Ace Alliance Report: The US iGaming Market Shows Signs of Decline

The US iGaming Market Is the World’s Largest

The US remains the largest iGaming market among the 135 countries tracked by Blask. Based on projected revenue measured through the Competitive Earning Baseline (CEB), the market was six times larger than its nearest competitor in the first half of 2026. Its H1 2026 CEB also exceeded the combined total of the next ten largest markets tracked by Blask.

Despite its size, the US iGaming market is no longer recording growth. The onshore segment led the decline, with CEB falling by 5.7% compared to H1 2025. Combined with the relative stability of the offshore segment, the data suggests that licensed operators are losing market share.

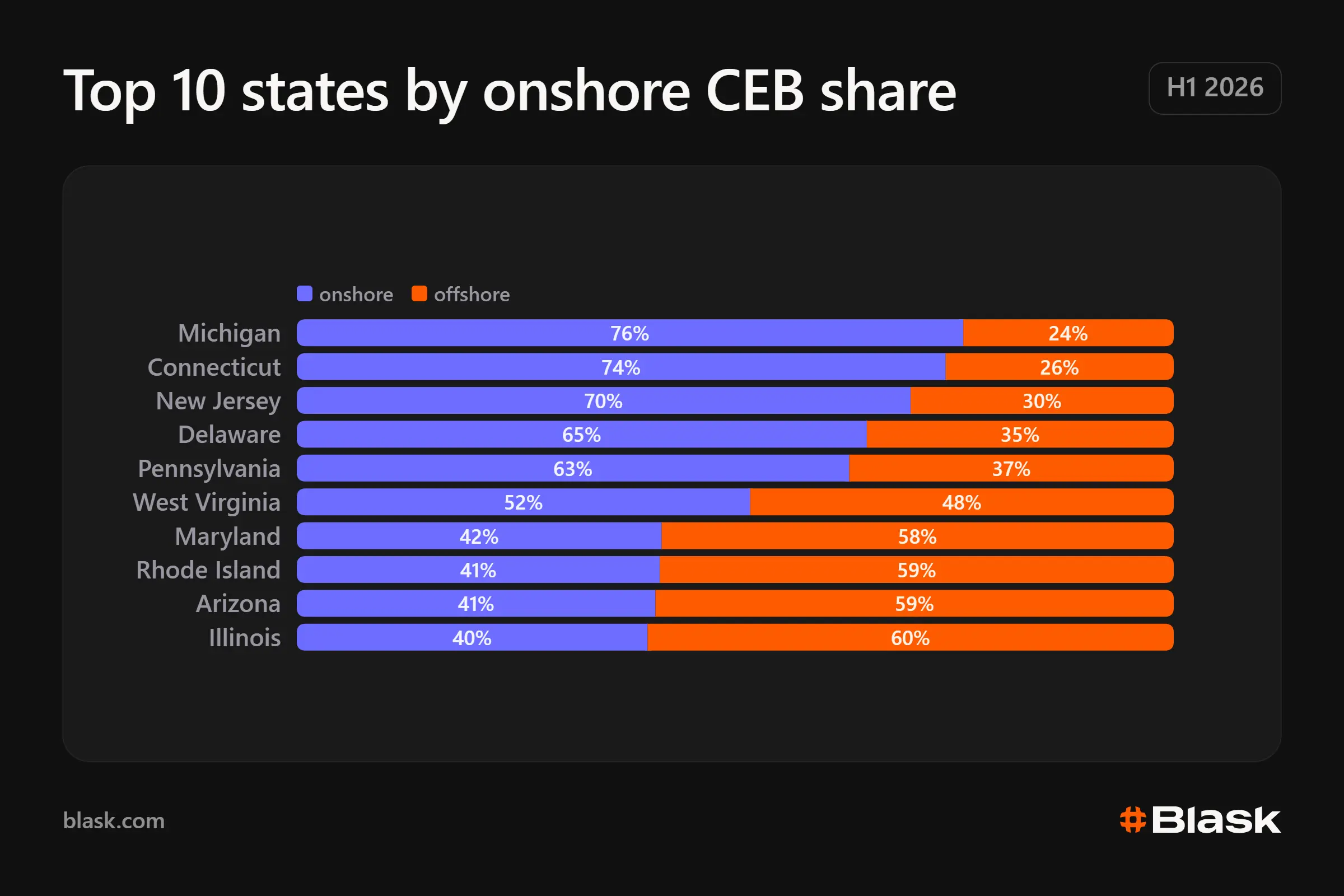

Onshore Operators Account for One-Third of US iGaming Market Revenue

In the first half of 2026, licensed operators accounted for 32.8% of projected US iGaming revenue, measured through Blask’s Competitive Earning Baseline (CEB). This was 1.4 percentage points lower than in H1 2025. The onshore share of user demand, measured by the Blask Index, remained broadly unchanged. However, demand for licensed operators fell by 8% in absolute terms as the wider US market contracted. Similar channelisation challenges were identified in the Blask x Ace Alliance analysis of World Cup 2026 iGaming demand across Europe, where regulation, product availability and market structure influenced how effectively licensed operators captured demand.

Within the US, channelisation was highest in states where both online casino gaming and sports betting are regulated. Rhode Island was the main exception, with its monopoly model generating an onshore CEB share of just 41.4% between January and June 2026. Across other fully regulated states, licensed operators accounted for between 51.7% of projected revenue in West Virginia and 76.3% in Michigan. New Jersey was the only fully regulated state where the onshore CEB share declined year over year, falling by 3.9 percentage points.

Among states where only online sports betting is legal, Maryland recorded the highest level of channelisation. Licensed operators accounted for 41.6% of the state’s CEB in H1 2026, although this share was 3.5 percentage points lower than a year earlier.

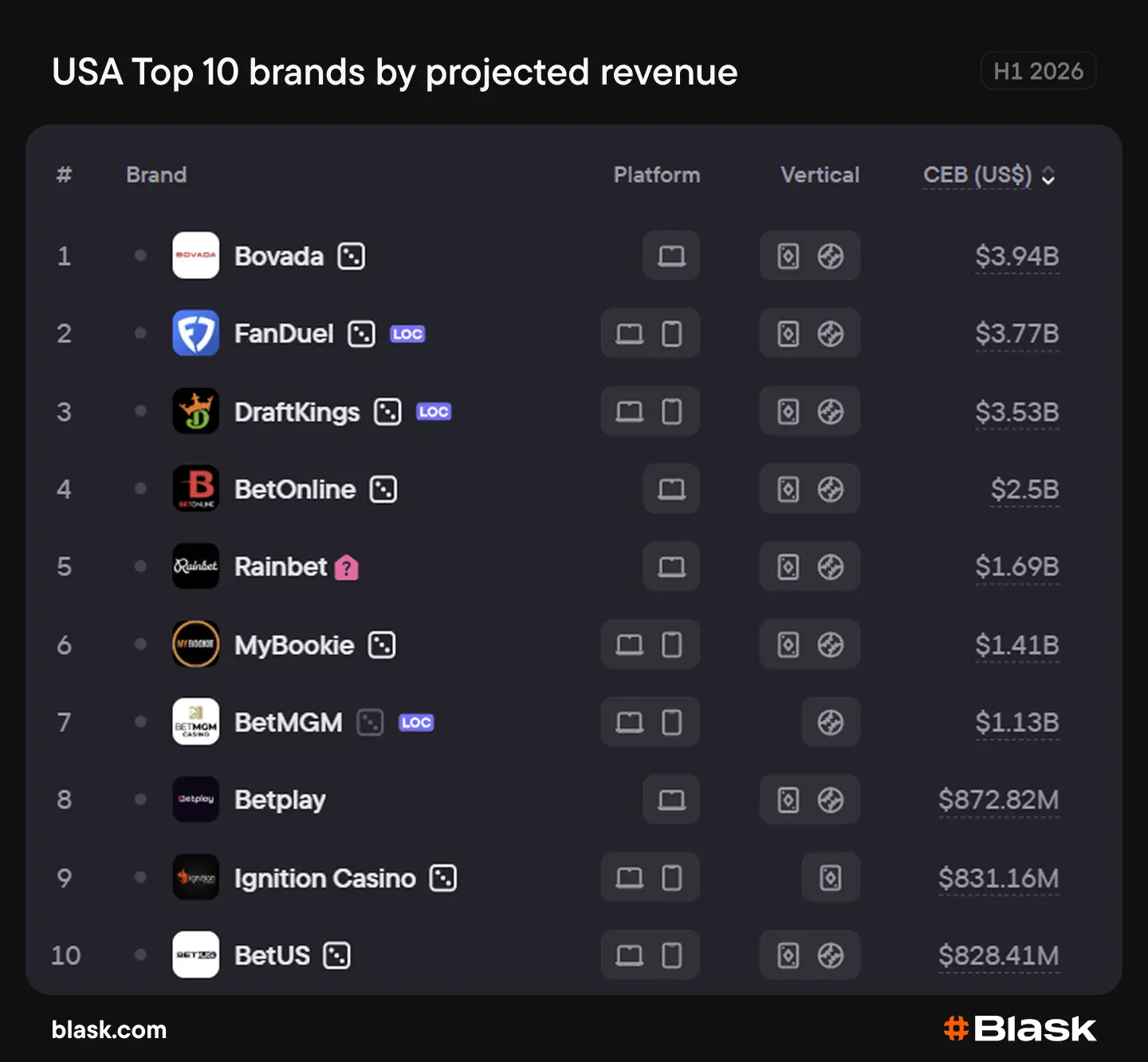

Offshore Brands Dominate the US iGaming Market

Seven of the ten largest US iGaming brands by projected revenue are offshore operators. Bovada remains the market leader, although licensed operators FanDuel and DraftKings are narrowing the gap.

Bovada’s Competitive Earning Baseline (CEB) fell by 4.1% in the first half of 2026 compared to H1 2025. FanDuel recorded a smaller decline of 1.3%, while DraftKings increased its CEB by 1.1%. The strongest growth among the top-ranked brands came from offshore operator BetOnline. Its CEB rose by 21.5% year over year, placing the brand fourth in the US market.

Bovada also maintained a substantial lead in user demand. Its Blask Index remained higher than the combined total recorded by FanDuel and DraftKings. However, demand for Bovada fell by 10.3% compared to H1 2025, while FanDuel recorded a steeper decline of 13.4%. DraftKings moved in the opposite direction, with its Blask Index increasing by 1.9%.

What the Data Shows About the US iGaming Market

The US remains the world’s largest iGaming market, but most activity continues to flow through offshore operators. Brands without a US licence account for around two-thirds of projected revenue and three-quarters of user demand.

Blask data indicates that the market lost momentum in the first half of 2026, with licensed operators recording a sharper decline than their offshore competitors. The findings suggest that the onshore segment is struggling to increase channelisation and capture a larger share of the market.

The US findings also provide a useful contrast with the Blask x Ace Alliance LATAM iGaming market report, where demand patterns were more closely shaped by local betting culture, regulation, payment infrastructure and World Cup cycles. Together, the regional reports show that market size alone does not determine whether licensed operators can capture and retain iGaming demand.